The Trillion Dollar Equation

This single equation spawned four multi-trillion dollar industries and transformed everyone's approach to risk.

10 capitulos

- The Power of Mathematical Prediction in MarketsCore ImpactA single equation spawned four multi-trillion dollar industries and fundamentally transformed how people approach risk in financial markets.Success Stories• Jim Simons created the Medallion Investment Fund in 1988, delivering 66% annual returns for 30 years • $100 invested in 1988 would be worth $8.4 billion today • Simons became the richest mathematician of all timeHistorical ContrastIsaac Newton, despite his mathematical genius, lost a third of his £30,000 wealth investing in the South Sea Company in 1720 because he couldn't predict human behavior.Key DifferenceThe most successful market traders were not veteran traders but physicists, scientists, and mathematicians who could model market dynamics mathematically.

- From Ancient Olives to Modern OptionsAncient OriginsThe Greek philosopher Thales of Miletus executed the first known call option around 600 BC by paying olive press owners to secure the right to rent their presses at a fixed price during the harvest season.How Options Work• A call option gives the right to buy something at a later date for a set strike price • A put option gives the right to sell something at a later date for the strike price • Options provide limited downside risk (you lose only the premium paid) but potentially large gainsStrategic Advantages• Limits downside losses to the premium paid • Provides leverage: a $10 option on $100 stock can yield 200% returns • Can be used as insurance to hedge against price movementsThe ChallengeFor hundreds of years, traders had no mathematical way to price options. They simply bargained to agree on a price, creating chaos on trading floors.

- Bachelier's Random Walk DiscoveryThe ProblemLouis Bachelier, working at the Paris Stock Exchange, realized that stock prices are influenced by countless unpredictable factors, making them impossible to forecast with certainty.The SolutionBachelier proposed that at any point in time, stock prices are equally likely to go up or down, and therefore follow a random walk like a coin flip, with expected future prices forming a normal distribution.Mathematical Foundation• Bachelier rediscovered the same equation Joseph Fourier used to describe heat radiation in 1822 • He called his discovery the 'radiation of probabilities' • His work laid the foundation for pricing options using probability calculationsRecognition GapWhen Bachelier finished his PhD, he had solved a centuries-old problem and beat Einstein to the random walk concept, but neither physicists nor traders noticed his work.

- Brownian Motion Connects Physics and FinanceThe MysteryScottish botanist Robert Brown observed in 1827 that microscopic particles suspended in water moved randomly, a phenomenon later called Brownian motion, but the cause remained unexplained for 80 years.Einstein's AnswerIn 1905, Einstein hypothesized that Brownian motion results from trillions of molecules hitting particles from every direction, with random imbalances causing observable movement.Mathematical Parallel• Einstein's derivation assumed particles move equally likely in any direction, just like stock prices • Particle location follows a normal distribution that widens over time • This explains diffusion even in still waterScientific ImpactBy solving the Brownian motion mystery, Einstein provided definitive evidence that atoms and molecules exist, unaware that Bachelier had discovered the same mathematics five years earlier.

- Thorpe's Blackjack Strategy Meets Wall StreetCasino Success• Ed Thorpe, a physics graduate, invented card counting by keeping mental track of played cards • He bet larger amounts when odds favored him and smaller amounts when they didn't • Casinos countered by adding more decks, reducing the advantage of card countingMarket ApplicationThorpe transferred his card-counting skills to the stock market, calling it the biggest casino on Earth, and started a hedge fund that achieved 20% annual returns for 20 years.Dynamic HedgingThorpe pioneered dynamic hedging, where an option seller owns stock to offset losses. If stock price rises, losses from the option are covered by stock gains, allowing risk-free profits with minimal fluctuation risk.Model ImprovementThorpe created a more accurate option pricing model than Bachelier's, accounting for stock price drift (the tendency of stocks to increase or decrease over time based on company performance).

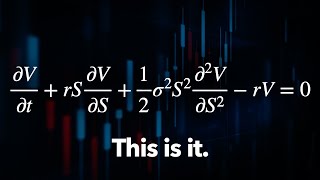

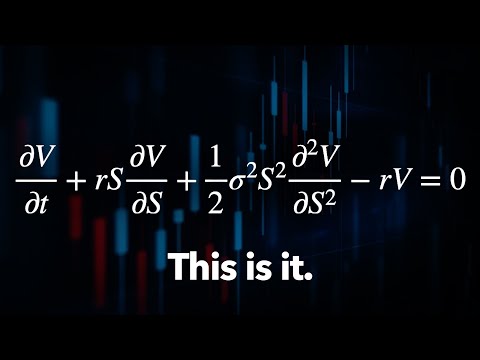

- Black-Scholes-Merton Equation Revolutionizes FinanceThe BreakthroughIn 1973, Fischer Black and Myron Scholes published an equation for option pricing, with Robert Merton independently publishing a version based on stochastic calculus, fundamentally changing the financial industry.Core PrincipleThey argued that a risk-free portfolio of options and stocks should return only the risk-free rate (US Treasury bond returns). This means fair option pricing balances risk between buyers and sellers equally.Practical Impact• The Chicago Board Options Exchange was founded the same year • The formula was adopted as the benchmark for Wall Street within a couple of years • Options market volume has doubled roughly every five years sinceIndustries Created• Exchange-traded options market (multi-trillion dollars) • Credit default swaps market • OTC derivatives market • Securitized debt market

- Real-World Applications of Options PricingCorporate Risk ManagementAirlines use options to hedge against oil price increases by pricing options to buy something tracking oil prices, which pay off when oil costs rise and compensate for higher fuel expenses.Leverage in Markets• With $1 of cash, you can buy $1 of stock • With $1 of cash, you can buy options affecting $10-20 of stock • This natural leverage in derivatives amplifies both gains and lossesGameStop ExampleReddit traders on r/wallstreetbets used options leverage to drive up GameStop stock prices, forcing hedge fund short sellers to lose money quickly by combining stock purchases with options that multiplied market impact.Market ImpactOptions enable hedging for companies, governments, and individual investors. They provide liquidity during normal times, but can exacerbate market crashes during periods of stress when all securities move in the same direction.

- The Scale of Derivatives MarketsMarket SizeGlobal derivatives markets are on the order of several hundred trillion dollars, representing multiples of the underlying securities they are based on.Why This WorksOptions allow a single underlying asset to be transformed into 5, 10, 20, or 50 different versions with varying risk-reward profiles that appeal to investors with different preferences.Stability Effects• During normal times: derivatives provide significant liquidity and stability • During market stress: all securities can move together in the same direction • In crashes: derivatives markets can exacerbate market dislocationsParadoxical OutcomeIf we ever discover all patterns in the stock market, knowing what they are will eliminate them. We would finally achieve a perfectly efficient market where all price movements are truly random.

- Jim Simons and the Medallion FundAcademic Foundation• Jim Simons was a world-class mathematician whose work on Riemann geometry influenced knot theory, quantum field theory, and quantum computing • Chern-Simons theory laid mathematical foundation for string theory • He received the Oswald Veblen Prize in geometry in 1976Strategic ApproachWhen founding Renaissance Technologies in 1978, Simons' strategy was to use machine learning to find patterns in the stock market, believing complexity prevents certainty but patterns provide opportunities.Team Building• Simons hired physicists, astronomers, mathematicians, and statisticians with PhDs and proven research records • He explicitly avoided people with finance backgrounds • He sought scientists who had done science well in their respective fieldsMedallion Success• Used hidden Markov models and data-driven strategies • Became the highest-returning investment fund of all time • Challenged the efficient market hypothesis itself

- Beyond the Efficient Market: Beating the SystemThe EvidenceIn 1988, Bradford Cornell published research showing that the efficient market hypothesis is false and that predictabilities exist in the stock market, based on the Medallion Fund's extraordinary performance.Requirements for SuccessIt is possible to beat the market if you have the right models, proper training, adequate resources, sufficient computational power, and advanced mathematical techniques.Pattern RecognitionPhysicists and mathematicians discovered patterns in stock markets and uncovered the randomness underlying them, providing new insights into risk and opening entirely new markets.Legacy Impact• Determined accurate prices for derivatives • Eliminated market inefficiencies • Demonstrated that mathematical modeling could revolutionize finance